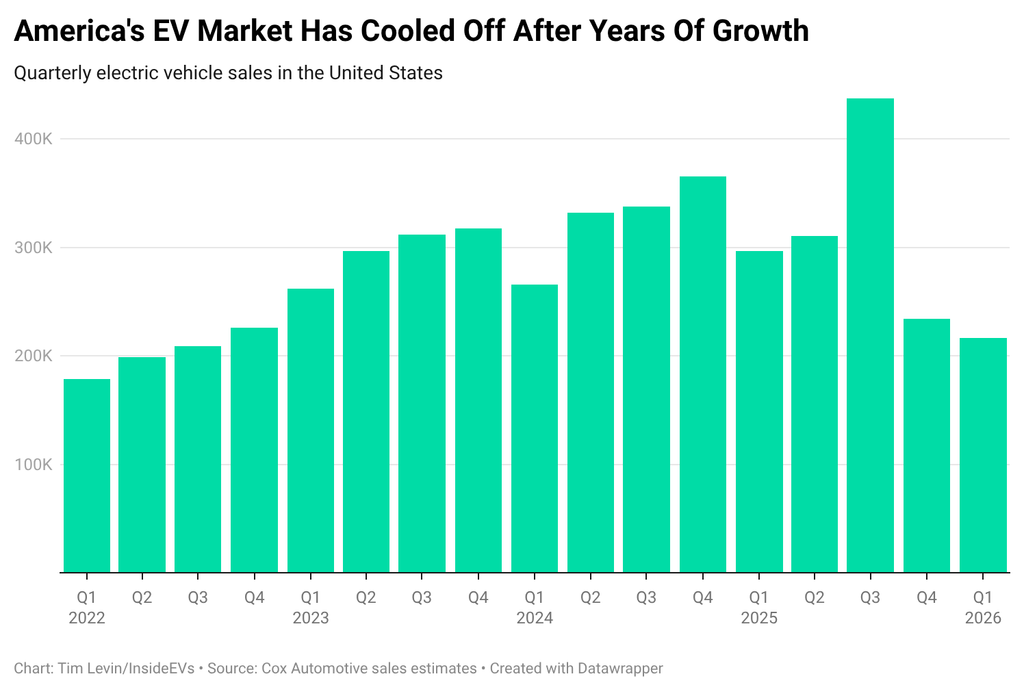

The United States electric vehicle (EV) market experienced a significant contraction during the first quarter of 2026, marking a turbulent start to the year for an industry that has long been touted as the future of American transportation. According to the latest data and estimates from Cox Automotive, American consumers purchased approximately 216,000 new electric vehicles between January and March. This figure represents a 27% decline on a year-over-year basis, continuing a downward trend that began in the latter half of 2025. This contraction follows a 36% drop in the fourth quarter of the previous year, effectively resetting the EV market’s quarterly sales volume to levels not seen since late 2022.

The downturn highlights a period of profound transition and "policy whiplash" that has fundamentally altered the purchasing landscape for zero-emission vehicles. As the industry grapples with the expiration of federal tax credits and a shifting regulatory environment, car manufacturers are being forced to find a "new normal" for consumer demand. This period of uncertainty has led several major automakers to delay or entirely cancel upcoming EV models, creating a secondary blow to sales as consumers find fewer options available on dealership lots.

A Chronology of the EV Market Shift

To understand the current state of the market, one must look at the timeline of events leading up to the Q1 2026 results. The industry saw a period of artificial inflation in the third quarter of 2025, driven by a consumer rush to take advantage of federal tax credits before their scheduled termination. During that period, EVs captured more than 10% of the total U.S. automotive market share. However, the subsequent removal of these incentives led to a 46% crash in sales during the fourth quarter of 2025.

By the start of 2026, the market appeared to be seeking a floor. While the 216,000 units sold in Q1 represent a year-over-year decline, analysts point to a quarter-over-quarter drop of only 7.8% as a sign of potential stabilization. For the last two quarters, the EV market share has remained relatively flat at approximately 6%. Cox Automotive analysts noted that while the numbers are lower than the peaks of 2025, the slowing rate of decline suggests that the initial shock of losing government-backed incentives may be subsiding.

The chronology of this market cooling is also tied to the production strategies of legacy automakers. In late 2025 and early 2026, several "Big Three" manufacturers shifted their focus back to internal combustion engine (ICE) vehicles and hybrids. This strategic pivot was a direct response to the removal of clean-car regulations that previously pressured companies to prioritize electric sales to meet fleet-wide emission standards.

Divergent Performance Across Major Brands

The first quarter of 2026 revealed a stark divide between manufacturers that have successfully navigated the new economic climate and those that have seen their electric portfolios crumble.

Stellantis, the parent company of brands such as Jeep, Dodge, and Fiat, faced a particularly grueling quarter. The company reported declines exceeding 80% across its core EV offerings, including the Fiat 500e, the Jeep Wagoneer S, and the Dodge Charger EV. Combined, these three models accounted for fewer than 500 units sold in the first three months of the year. Similarly, Audi’s electric vehicle sales plunged by nearly 90%, and Honda saw a 65% decrease.

Kia, which had previously been a strong contender in the EV space, saw sales drop by nearly 40%. The company indicated that it has intentionally prioritized the production of combustion vehicles at facilities that utilize flexible assembly lines for both gas and electric cars. Chevrolet also faced a 30% decline; while the Equinox EV maintained a respectable presence, the more expensive Blazer EV saw its sales volume fall from over 5,000 units to just over 1,000 vehicles.

Conversely, a few brands managed to buck the downward trend. Cadillac saw a 20% increase in EV sales, attributed to a rapidly expanding and diversifying lineup that appealed to luxury buyers less sensitive to the loss of tax credits. Rivian also reported year-over-year growth, maintaining its position as a resilient "pure-play" EV manufacturer. Hyundai managed to keep its sales flat, but only through aggressive tactical moves, such as slashing the price of the popular Ioniq 5 by nearly $10,000 to remain competitive in a price-sensitive market.

The Tesla Paradox and Market Concentration

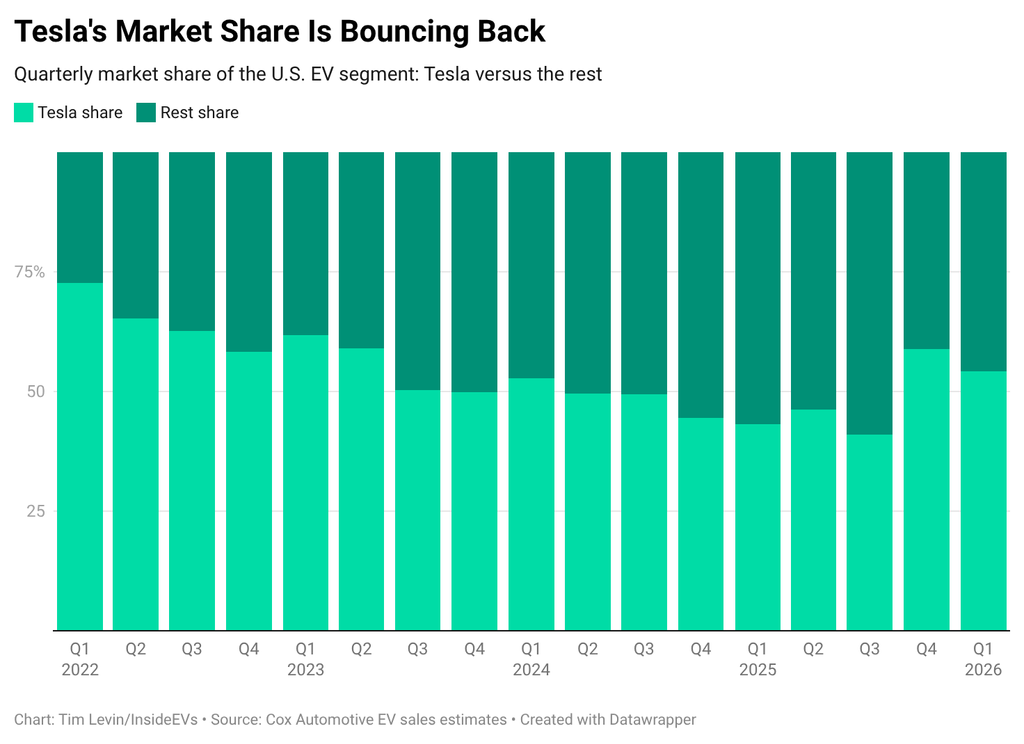

Tesla remains the dominant force in the U.S. EV market, but its role in the Q1 2026 landscape is complex. For several years, Tesla’s market share had been eroding as legacy automakers entered the space. However, as the overall market contracted in early 2026, Tesla actually regained a larger slice of the pie.

In the first quarter of 2026, Tesla claimed 54.2% of all U.S. electric vehicle sales, a significant jump from the 43.2% share it held during the same period in 2025. This resurgence in market share occurred despite the fact that Tesla’s own U.S. sales fell by 8.4%. The company’s increased concentration is largely due to the fact that its competitors’ sales fell much more drastically.

Tesla’s ability to weather the end of tax credits better than its rivals stems from two primary factors. First, unlike legacy manufacturers, Tesla does not have a profitable internal combustion business to retreat to; it must sell EVs to survive. Second, Tesla’s long-standing focus on manufacturing efficiency has allowed its vehicles to remain profitable even at lower price points, whereas many legacy brands were relying on subsidies to offset the high costs of their nascent EV programs. Nevertheless, it was a difficult quarter for the Austin-based company, as the Model 3 recorded its worst quarterly performance in years, hampered by logistics issues and shifting consumer preferences.

Toyota’s Strategic Ascent

One of the most surprising developments of the first quarter was the performance of Toyota. After years of being criticized by environmental advocates for a perceived "slow" entry into the battery-electric market, Toyota’s "fast-follower" strategy appears to be yielding results.

Sales of the Toyota bZ crossover nearly doubled year-over-year, surpassing 10,000 units in Q1. This surge propelled the bZ to become the best-selling non-Tesla EV in the United States, snatching the title from the Chevrolet Equinox EV. Toyota’s success has been attributed to a combination of aggressive dealer incentives and significant technical improvements made for the 2026 model year. By prioritizing hybrids while slowly scaling its fully electric offerings, Toyota has positioned itself to capture buyers who are looking for value and reliability rather than cutting-edge early adoption.

Economic Headwinds and Geopolitical Factors

The broader economic environment has played a critical role in the cooling of the EV market. High interest rates throughout early 2026 have made the higher upfront costs of electric vehicles more difficult for the average consumer to finance. Furthermore, geopolitical instability has introduced new variables.

The ongoing conflict involving Iran has led to fluctuations in global oil prices. While high gas prices traditionally nudge consumers toward electric vehicles, the broader economic impact of energy uncertainty—such as increased shipping costs and inflation—has dampened overall consumer confidence. In this environment, many buyers are opting for "safe" choices, such as traditional hybrids, rather than making the leap to full electrification.

Additionally, the used EV market is beginning to exert pressure on new vehicle sales. A flood of modern, off-lease electric cars has hit the secondary market, offering price-conscious buyers a way to go electric at a fraction of the cost of a new 2026 model. While this transition is positive for the overall adoption of zero-emission technology, it creates a "slow burn" effect that can cannibalize the sales of new, high-margin electric models.

Future Outlook and Market Implications

As the industry looks toward the remainder of 2026, the trajectory of the EV market will depend heavily on the strategic decisions of automakers and the potential for renewed regulatory support.

Several highly anticipated models are slated for release later this year, including the BMW iX3 and the Rivian R2. These vehicles are expected to inject "new energy" into the market, targeting segments that have remained underserved. Industry analysts suggest that if these models can hit their promised price points and performance metrics, they could improve both sales volumes and the general "vibe" surrounding the electric transition.

However, the road ahead remains steep. The industry is currently in the "chasm" of the technology adoption curve, moving from early adopters to the more skeptical mass market. To bridge this gap, manufacturers will likely need to continue sacrificing profit margins to offer competitive pricing, at least until battery costs further decline.

Long-term growth is still projected, driven by the inevitable improvement in charging infrastructure—exemplified by the Ionna joint venture and its partnership with Circle K—and the eventual return of federal or state-level incentives. For now, the Q1 2026 results serve as a sobering reminder that the transition to an all-electric fleet is not a linear progression, but a complex evolution shaped by policy, economics, and the practical realities of the American consumer.

{kind=link}

{kind=link}