The recent surge in gasoline prices across the United States has once again ignited a national conversation regarding the pace of the transition to electric vehicles (EVs). While historical logic suggests that pain at the pump serves as a primary catalyst for consumers to abandon internal combustion engines, the current economic and political landscape presents a far more nuanced reality. Despite prices exceeding $4 per gallon in several regions—a threshold that traditionally triggers a shift in consumer sentiment—a combination of policy reversals, high interest rates, and a lack of affordable models has created a disconnect between fuel costs and EV adoption rates.

The Economic Disconnect: Why High Gas Prices Are Not a Silver Bullet

For decades, energy economists have tracked the correlation between rising fuel costs and the demand for more efficient transportation. However, recent research suggests that the immediate impact of gas price spikes on the automotive market is often overstated. Joshua Linn, an economist at the University of Maryland and a senior fellow at Resources for the Future, has conducted extensive studies on the relationship between fuel prices and vehicle fleet efficiency. His findings indicate that while consumers do shift toward more fuel-efficient options when gasoline costs rise, the overall impact on the national average fuel economy is relatively modest.

According to Linn’s research, a $1 increase in the price of a gallon of gasoline typically results in an average fuel economy increase of only about one mile per gallon across the new vehicle fleet. This is largely because the automotive market is characterized by slow turnover; most consumers only purchase a new or used vehicle every several years, meaning they are "locked in" to their current vehicle’s fuel consumption regardless of short-term price fluctuations.

Furthermore, for a price spike to fundamentally alter buying habits, it must be perceived as permanent. David Reichmuth, research director for the clean transportation program at the Union of Concerned Scientists, notes that if consumers believe prices will stabilize within a few months, they are less likely to make the significant financial leap to an electric vehicle. This "wait and see" approach is compounded by the fact that high gasoline prices act as a regressive tax, leaving households with less disposable income to put toward the higher upfront cost of an EV.

A Chronology of Policy Shifts and Market Cooling

The U.S. EV market is currently navigating a period of significant cooling, following a peak in 2025. This downturn can be traced back to a series of specific policy changes and strategic pivots by major automakers.

In October 2025, a significant shift in federal policy occurred when the existing tax credits for electric vehicles were eliminated. Previously, consumers could access up to $7,500 for the purchase of a new EV and $4,000 for a used model. The removal of these incentives, combined with a period of high interest rates, significantly increased the total cost of ownership for prospective buyers.

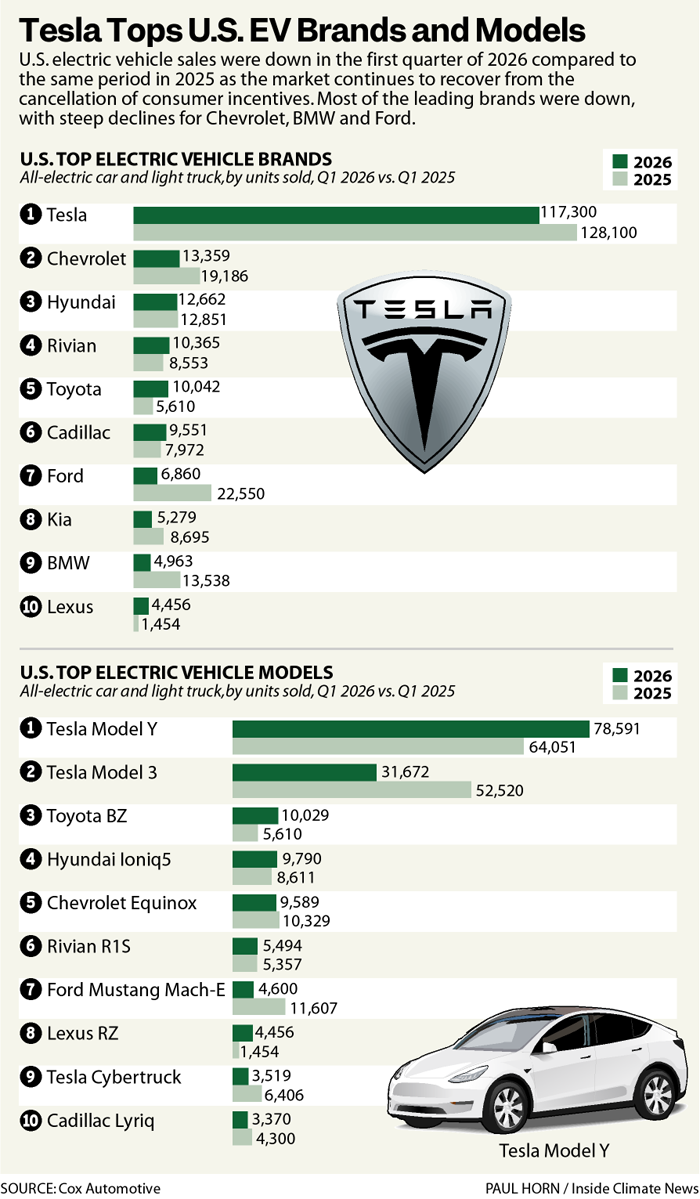

The impact of these changes became starkly evident in the first quarter of 2026. Data from Cox Automotive reveals that U.S. electric vehicle sales plummeted by 27 percent compared to the same period in 2025. Perhaps more tellingly, the EV market share of all U.S. car and light truck sales dropped to 5.8 percent, a sharp decline from the peak of 10.6 percent recorded just a year prior.

In response to this perceived softening of demand, several major automakers have retrenched:

- Honda: The company recently halted plans for three U.S.-manufactured EV models that were intended to showcase its next-generation technology.

- General Motors: GM announced that the revamped Chevrolet Bolt EV—one of the most affordable options on the market—will have a limited production run of approximately 18 months before production ends in 2027.

- Volkswagen: The German automaker confirmed it would cease sales of the ID.4 in the United States, effectively removing its primary EV offering from the American market.

The Global Context: China’s Rise as an "Electrostate"

While the U.S. market faces domestic headwinds, the global transition to electric mobility continues at a rapid pace, with China emerging as the dominant force. Unlike the United States, where EV sales have fluctuated, global sales reached 1.75 million units in March 2026 alone, driven largely by growth in Europe and Asia.

China has strategically positioned itself as an "electrostate," leveraging its control over the battery supply chain and manufacturing infrastructure to produce affordable EVs at scale. This dominance has significant geopolitical implications, particularly as the conflict in the Middle East continues to highlight the risks of oil dependency. As nations seek energy security through wind, solar, and battery storage, they increasingly find themselves reliant on Chinese-manufactured components.

Ford CEO Jim Farley recently addressed this competitive pressure, noting that Chinese automakers have the capacity to disrupt the U.S. manufacturing economy if left unchecked. Currently, high tariffs prevent Chinese EVs from entering the U.S. market in significant numbers, but Farley acknowledged that domestic manufacturers must innovate rapidly to remain competitive. "Manufacturing is the heart and soul of our country," Farley stated in a recent interview, emphasizing that Ford and its peers must produce vehicles that are fully competitive with Chinese offerings in terms of both technology and price.

Domestic Infrastructure and Regulatory Hurdles

Beyond the automotive market, the broader energy transition in the United States is facing localized challenges. In Maine, the state legislature recently passed a first-of-its-kind moratorium on large-scale data centers. The bill, which pauses development until October 2027, reflects growing concerns over the massive electricity and water demands of the tech industry. As data centers proliferate to support artificial intelligence and cloud computing, they threaten to strain aging power grids and compete with the energy needs of residential and industrial sectors.

This legislative move in Maine is expected to set a precedent, with at least a dozen other states considering similar pauses. These developments underscore a critical tension in the energy transition: while the demand for clean electricity is rising, the infrastructure required to support that demand—and the industries that consume it—is under increasing scrutiny.

Milestones in Renewable Generation

Despite the hurdles in the EV sector, the U.S. power sector reached a historic milestone in March 2026. For the first time in the history of the modern grid, renewable energy sources—including wind, solar, and hydroelectric power—generated more electricity than natural gas or any other single source.

While this achievement was partly due to seasonal factors—March typically sees lower overall electricity demand, allowing grid operators to throttle back coal and gas plants—it serves as a proof of concept for a decarbonized grid. Energy analysts predict that while it may take several years for renewables to outpace natural gas on an annual basis, the trend line is clear. The growth of utility-scale battery storage is expected to further stabilize this transition, allowing renewable energy to be deployed even when the sun is not shining or the wind is not blowing.

Regional Friction: The California Example

The complexities of the energy transition are perhaps most visible in California, a state that has long positioned itself as a global leader in climate policy. At a recent climate summit, activists and industry leaders expressed frustration with the pace of progress. Governor Gavin Newsom has faced criticism from environmental advocates who argue that his administration has not moved aggressively enough to phase out fossil fuels or support decentralized solar energy.

The friction in California highlights the "growing pains" of the clean energy shift. As states move from setting ambitious goals to implementing specific projects, they must navigate land-use disputes, supply chain bottlenecks, and the political fallout of rising utility costs.

Looking Ahead: Fundamentals vs. Policy

As the U.S. moves through the remainder of 2026, the trajectory of the EV market will likely depend on whether "fundamentals" can overcome the loss of policy support. Stephanie Valdez Streaty, director of insights at Cox Automotive, suggests that the market is moving into a phase driven less by government incentives and more by the inherent value proposition of electric technology.

For long-term growth to resume, the U.S. market requires a broader range of affordable models and a more robust, reliable charging infrastructure. The current "sales swoon" may be a temporary correction as the industry recalibrates to a post-subsidy environment. However, with gasoline prices remaining volatile and global competition intensifying, the pressure on U.S. policymakers and automakers to find a sustainable path forward has never been greater. The transition is no longer just about environmental stewardship; it is increasingly a matter of economic competitiveness and national energy security.

{kind=link}

{kind=link}